Fitch Ratings-London: GCC banks are benefitting from strong operating conditions supported by high oil prices, contained inflation and rising interest rates, but bank performance varies between markets, Fitch Ratings says. UAE banks’ profitability has improved significantly, in contrast to that of Saudi and Qatari banks. We expect this improvement to be overall sustained, which, along with other solid financial metrics being maintained, could lead to positive rating actions on some UAE banks’ Viability Ratings.

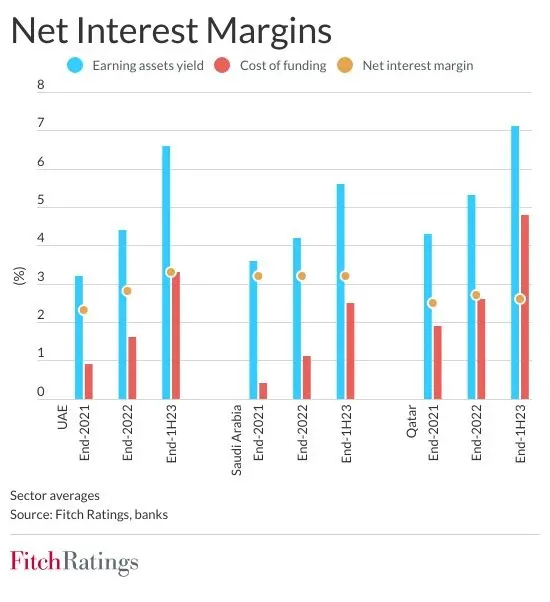

Banks in the main GCC markets, Saudi Arabia, Qatar and the UAE, are geared positively towards rising interest rates. Most loan books reprice fairly quickly, while low-cost current and savings accounts (CASA) deposits represent a significant proportion of funding. UAE banks have benefitted the most from rising rates, with average net interest margins (NIMs) 100bp higher in 1H23 than in 2020, compared with an 11bp increase for Qatari banks and little change for Saudi banks. As a result, UAE bank NIMs are now level with Saudi bank NIMs.

As we highlighted in July 2022, UAE banks are benefitting from healthy liquidity conditions, reflected in negative EIBOR-SAIBOR spreads. Liquidity is supported by high oil prices, foreign capital inflows and only moderate credit demand amid rising interest rates. We believe UAE bank NIMs have now peaked and will remain stable in 2H23, before declining slightly in 2024.

The lack of improvement in Saudi bank NIMs is mainly due to tighter liquidity, with financing growth in 2022 (14%) outpacing deposit growth (9%). Financing growth has largely been funded by term deposits, which cost more than CASA deposits. Liquidity pressure moderated in 1H23 as financing growth slowed to 5%, and we expect NIMs to increase moderately in 2H23. However, Saudi bank financing growth is likely to be above the GCC average in 2023–2024 due to increasing corporate credit demand, and, with interest rates still high, we expect pressure on liquidity to prevent NIMs from rising much above 2H23 levels.

Qatari bank NIMs have improved only slightly, reflecting a higher reliance on price- and confidence-sensitive non-domestic funding. CASA deposits account for only 20% of sector funding, compared with over 50% in the UAE and Saudi Arabia. New regulations penalising non-resident deposits in Basel III liquidity ratio calculations have increased competition for resident deposits, adding to funding costs, and the ability to pass higher rates to customers is hampered by exposures to highly indebted sectors. NIMs are also dampened by weak credit demand and by the public sector continuing to repay its overdraft facilities. We expect NIM improvement to be minimal in 2H23 and 2024 as strong competition limits banks’ ability to reprice assets.

In the UAE and Saudi Arabia, asset quality metrics were stable in 1H23, supported by strong operating conditions. The average cost of risk in both countries has decreased since end-2021, but could increase in 2H23 and 2024 (although not to 2021 levels) as higher interest rates affect credit performance, particularly given recent fast growth in Saudi bank financing. UAE mortgage portfolios could be pressured given their high proportion of variable-rate loans, but the rise in property prices should keep losses-given-default close to nil.

In Qatar, the average annualised cost of risk was stable in 1H23 (106bp), but remains elevated due to muted credit growth and continued provisioning against vulnerable exposures in the real estate and construction sectors. It may increase given an average Stage 2 loans ratio above 10% and low specific Stage 2 coverage but we believe overall provisioning is adequate.

Weaker global growth and lower-than-expected oil prices are key risks for all GCC banking sectors. Fitch forecasts oil prices to average USD80/barrel and USD75/barrel in 2023 and 2024, respectively, which should remain supportive of operating conditions.

The above article originally appeared as a post on the Fitch Wire credit market commentary page. The original article can be accessed at www.fitchratings.com. All opinions expressed are those of Fitch Ratings.

-Ends-

Disclaimer:

All Fitch Ratings (Fitch) credit ratings are subject to certain limitations and disclaimers. Please read these limitations and disclaimers by following this link: https://www.fitchratings.com/understandingcreditratings. In addition, the following https://www.fitchratings.com/rating-definitions-document details Fitch's rating definitions for each rating scale and rating categories, including definitions relating to default. Published ratings, criteria, and methodologies are available from this site at all times. Fitch's code of conduct, confidentiality, conflicts of interest, affiliate firewall, compliance, and other relevant policies and procedures are also available from the Code of Conduct section of this site. Directors and shareholders’ relevant interests are available at https://www.fitchratings.com/site/regulatory. Fitch may have provided another permissible or ancillary service to the rated entity or its related third parties. Details of permissible or ancillary service(s) for which the lead analyst is based in an ESMA- or FCA-registered Fitch Ratings company (or branch of such a company) can be found on the entity summary page for this issuer on the Fitch Ratings website.

In issuing and maintaining its ratings and in making other reports (including forecast information), Fitch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of Fitch's factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third- party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of Fitch's ratings and reports should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information Fitch relies on in connection with a rating or a report will be accurate and complete. Ultimately, the issuer and its advisers are responsible for the accuracy of the information they provide to Fitch and to the market in offering documents and other reports. In issuing its ratings and its reports, Fitch must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings and forecasts of financial and other information are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings and forecasts can be affected by future events or conditions that were not anticipated at the time a rating or forecast was issued or affirmed.

The information in this report is provided 'as is' without any representation or warranty of any kind, and Fitch does not represent or warrant that the report or any of its contents will meet any of the requirements of a recipient of the report. A Fitch rating is an opinion as to the creditworthiness of a security. This opinion and reports made by Fitch are based on established criteria and methodologies that Fitch is continuously evaluating and updating. Therefore, ratings and reports are the collective work product of Fitch and no individual, or group of individuals, is solely responsible for a rating or a report. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. All Fitch reports have shared authorship. Individuals identified in a Fitch report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at any time for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from US$1,000 to US$750,000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from US$10,000 to US$1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of the United Kingdom, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution, Fitch research may be available to electronic subscribers up to three days earlier than to print subscribers.

For Australia, New Zealand, Taiwan and South Korea only: Fitch Australia Pty Ltd holds an Australian financial services license (AFS license no. 337123) which authorizes it to provide credit ratings to wholesale clients only. Credit ratings information published by Fitch is not intended to be used by persons who are retail clients within the meaning of the Corporations Act 2001.

Fitch Ratings, Inc. is registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization (the 'NRSRO'). While certain of the NRSRO's credit rating subsidiaries are listed on Item 3 of Form NRSRO and as such are authorized to issue credit ratings on behalf of the NRSRO (see https://www.fitchratings.com/site/regulatory), other credit rating subsidiaries are not listed on Form NRSRO (the 'non-NRSROs') and therefore credit ratings issued by those subsidiaries are not issued on behalf of the NRSRO. However, non-NRSRO personnel may participate in determining credit ratings issued by or on behalf of the NRSRO.

Copyright © 2023 by Fitch Ratings, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, NY, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved.

Matt Pearson

Senior Associate, Corporate Communications

Fitch Group, 30 North Colonnade, London, E14 5GN

E: matthew.pearson@thefitchgroup.com