PHOTO

- Sustained growth in new business and total activity

- Input price inflation retreats from October's four-year high

Doha, Qatar – The latest Purchasing Managers’ Index™ (PMI®) survey data from Qatar Financial Centre (QFC) compiled by S&P Global signalled another solid improvement in business conditions in Qatar's non-energy private sector in November. Demand for goods and services increased further, supporting growth in total activity. The 12-month outlook for activity remained stronger than the long-run survey trend as firms mentioned Qatar's attractiveness to international investment. The labour market remained very strong, with another near-record increase in employment and sharp wage inflation as firms sought to attract and retain experienced staff. Overall cost inflation retreated from October's four-year high while firms continued to cut their own prices to boost competitiveness.

The Qatar PMI indices are compiled from survey responses from a panel of around 450 private sector companies. The panel covers the manufacturing, construction, wholesale, retail, and services sectors, and reflects the structure of the non-energy economy according to official national accounts data.

The headline Qatar Financial Centre PMI is a composite single-figure indicator of non-energy private sector performance. It is derived from indicators for new orders, output, employment, suppliers’ delivery times and stocks of purchases.

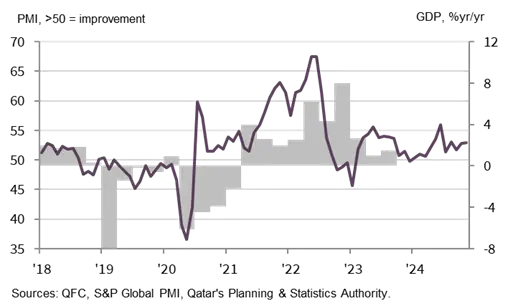

The PMI edged up to 52.9 in November, from 52.8 in October, signalling stronger overall growth in business conditions in the non-energy private sector economy. The rise in the headline figure in the latest survey took it further above the long-run survey average of 52.3 (since April 2017).

The rise in the PMI since October mainly reflected a faster increase in business activity, a survey-record increase in stocks of purchases and a softer improvement in suppliers' delivery times. Inflows of new business expanded for the eleventh month running, linked to improving market conditions, marketing efforts, and developing client relationships. Outstanding business decreased for the first time in three months as capacity was expanded.

Qatar's non-energy private sector labour market remained very strong in November. Over the past three months employment has risen more quickly than at any other time in the survey history. This was accompanied by further strong wage inflation, with November's increase the third-fastest on record following on from September and October. Companies reported boosting salaries to retain experienced and skilled staff in a highly competitive market. Overall cost pressures remained strong but eased from October's four-year high. In contrast, prices charged for goods and services fell for the fourth month running as firms sought to raise competitiveness.

Qatari firms maintained an optimistic outlook for the next 12 months in November. The strength of sentiment was broadly in line with the strong long-run survey trend since 2017. Positive forecasts were linked to domestic economic development, investment, population growth and demand in the real estate and construction sectors.

QFC Qatar PMI vs. GDP

Financial Services

Financial services continues to expand in November

- Further increases in new business and total activity

- Finance firms cut prices at the fastest rate on record

- Employment continues to rise sharply

Demand for Qatari financial services increased further in November, driving a marked increase in employment in the sector. Total activity rose again, with the seasonally adjusted Financial Services Business Activity Index remaining well above the no-change mark of 50.0 at 53.7, albeit down from 56.7 in October.

Companies were strongly optimistic regarding the 12-month outlook, although sentiment was slightly softer than the long-run series trend (since 2017).

Financial services companies cut their prices charged for the fourth month running, and at the fastest rate on record. Meanwhile, average input prices rose at the slowest rate in three months.

Comment

Yousuf Mohamed Al-Jaida, Chief Executive Officer, QFC Authority:

"The headline PMI edged up to 52.9 in November, surpassing the third quarter average of 52.0 and the long-run trend level of 52.3, indicating stronger business conditions in the non-energy sector.

"New business and output expanded further, while the labour market remained robust. Over the past three months, the Employment Index has registered the highest levels in the survey history. Demand for workers and efforts to retain experienced staff have been reflected in the survey data for wages, with the Staff Costs Index remaining higher than at any time prior to August.

"Overall cost pressures remained high, although the Input Prices Index retreated notably from October's four-year high. Despite this, the prices charged for goods and services fell, as firms continue to discount their prices to boost competitiveness."

-Ends-

ABOUT THE QATAR FINANCIAL CENTRE

The Qatar Financial Centre (QFC) is an onshore business and financial centre located in Doha, providing an excellent platform for firms to do business in Qatar and the region. The QFC offers its own legal, regulatory, tax and business environment, which allows up to 100% foreign ownership, 100% repatriation of profits, and charges a competitive rate of 10% corporate tax on locally sourced profits.

The QFC welcomes a broad range of financial and non-financial services firms.

For more information about the permitted activities and the benefits of setting up in the QFC, please visit qfc.qa

@QFCAuthority | #QFCMeansBusiness@QFCAuthority | #QFCMeansBusiness

MEDIA CONTACTS

QFC: Rasha Kamaleddine, Marketing & Corporate Communications Department, r.kamaleddine@qfc.qa

ENQUIRIES ABOUT THE REPORT

QFC: qatarpmi@qfc.qa

ABOUT S&P GLOBAL

S&P Global (NYSE: SPGI) S&P Global provides essential intelligence. We enable governments, businesses and individuals with the right data, expertise, and connected technology so that they can make decisions with conviction. From helping our customers assess new investments to guiding them through ESG and energy transition across supply chains, we unlock new opportunities, solve challenges, and accelerate progress for the world.

We are widely sought after by many of the world’s leading organizations to provide credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help the world’s leading organizations plan for tomorrow, today. www.spglobal.com.

ABOUT PMI

Purchasing Managers’ Index™ (PMI®) surveys are now available for over 40 countries and for key regions including the Eurozone. They are the most closely watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends.

www.spglobal.com/marketintelligence/en/mi/products/pmi.html

METHODOLOGY

The Qatar Financial Centre PMI® is compiled by S&P Global from responses to questionnaires sent to purchasing managers in a panel of around 450 private sector companies. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP. The sectors covered by the survey include manufacturing, construction, wholesale, retail, and services.

Survey responses are collected in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses. The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

The headline figure is the Purchasing Managers’ Index™ (PMI). The PMI is a weighted average of the following five indices: New Orders (30%), Output (25%), Employment (20%), Suppliers’ Delivery Times (15%) and Stocks of Purchases (10%). For the PMI calculation the Suppliers’ Delivery Times Index is inverted so that it moves in a comparable direction to the other indices.

Underlying survey data are not revised after publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series.

Data were collected 12-22 November 2024.

For further information on the PMI survey methodology, please contact economics@spglobal.com.

CONTACT

S&P Global: Sabrina Mayeen | E. Sabrina.mayeen@spglobal.com