PHOTO

- While Ukraine and Russia are remote from the region and linkages are not direct nor easy to identify, they give their views on how local economies are faring amid the volatility.

Key Points:

- Improving economic activity due to a proactive and robust pandemic response and a relatively better position against rising inflation compared to other markets has benefited the MENA region this year.

- Policymakers continue to press on with fiscal and economic reforms as well as environmental, social and governance (ESG) initiatives.

- Gulf Cooperation Council (GCC) bonds are generally of high quality and have defensive characteristics due to lower correlation, lower volatility and smaller drawdowns than their emerging market peers.

- MENA equity valuations are trading at a premium over other emerging markets, but have been supported by increasing earnings growth.

Proactive Pandemic Response Boosts Economic Activity

MENA governments were proactive in establishing a proper framework and guidelines to deal with COVID-19 early on, having initiated aggressive vaccine rollouts. The United Arab Emirates (UAE) leads the way, boasting a vaccine rate of more than 95% for a two-dose protocol.1 The remainder of GCC countries are expected to roll out their vaccines to 90% of the population by year-end. Proactive handling of the pandemic has allowed for economic activity to return gradually and on a more sustainable footing. We believe this momentum will carry forward through 2022 as economies continue to recover.

Strong Position Amid Concerns About Geopolitics, Oil Prices and Interest Rates

The MENA region has benefited from higher oil prices, driven by the Russia-Ukraine war, concerns around the Iranian nuclear talks and a significant drop in oil supply during the pandemic. Russia is likely to remain under sanctions and companies may continue to impose their own self-sanctions, whereby they refuse to do business with the country, even if the war ends. Substantial new investments will be required to compensate for the decline in existing oil fields to meet demand. We therefore expect oil prices to remain elevated over the medium term.

Likewise, global inflation expectations remain elevated, and markets have priced in several interest-rate hikes for the rest of this year. Unlike many markets where there is a risk of rising inflation alongside muted growth, in our opinion, inflation remains well-anchored across the GCC given currency pegs and a strong dollar, while growth continues to trend up.

Policymakers Committed to Reform Programs

One of the risks of higher oil prices is the possible pullback in the impressive pace of economic and fiscal reform in the MENA region. To address imbalances, policymakers have been diversifying their sources of revenue by introducing taxation and reining in spending and subsidies.

Given the Russia-Ukraine war and concerns about energy and food security, there is a risk that some of the net-zero targets and other long-term initiatives could be rolled back. However, we think policies are clear and decisions have already been made to be part of the solution as the world transitions to low carbon. ESG disclosures have been improving in the MENA region, with the UAE and Egypt making ESG disclosures mandatory. Saudi Arabia’s guidelines in this area should also be released by the end of the year, and its sovereign wealth fund has announced plans to issue green bonds soon.

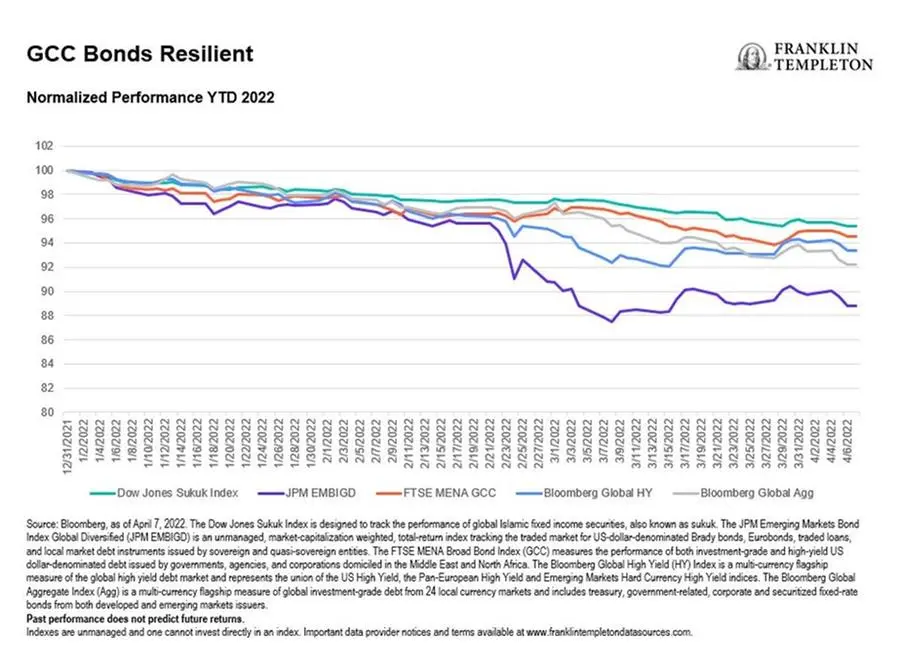

GCC Bonds’ Defensive Characteristics

In our opinion, GCC bonds are a higher-quality part of the emerging markets universe and exhibit important defensive characteristics. They have historically had a much lower level of correlation to other traditional asset classes and lower volatility compared to other fixed income sectors. Year-to-date, the global Sukuk market’s performance, as measured by the Dow Jones Sukuk Index, and the GCC market, as measured by the FTSE MENA GCC Index, held up well compared with the broad credit indexes.2 It is worth noting that the GCC represents approximately 70% of the Sukuk index. Over the past three years, GCC bonds have held on to gains, unlike emerging markets. Drawdowns have also historically been significantly less for the GCC during times of market stress compared to emerging markets.

In terms of issuance, given that the region is moving out of a budget deficit to a surplus, GCC bonds could lose market share relative to other emerging markets. However, this year emerging markets are generally expected to issue slightly less, and GCC bond issuance, while less than last year, should still be roughly 30% of overall emerging market issuance.3 Less issuance could also be slightly supportive for bond prices going forward.

MENA Equities Benefiting from Inflows and Earnings Growth

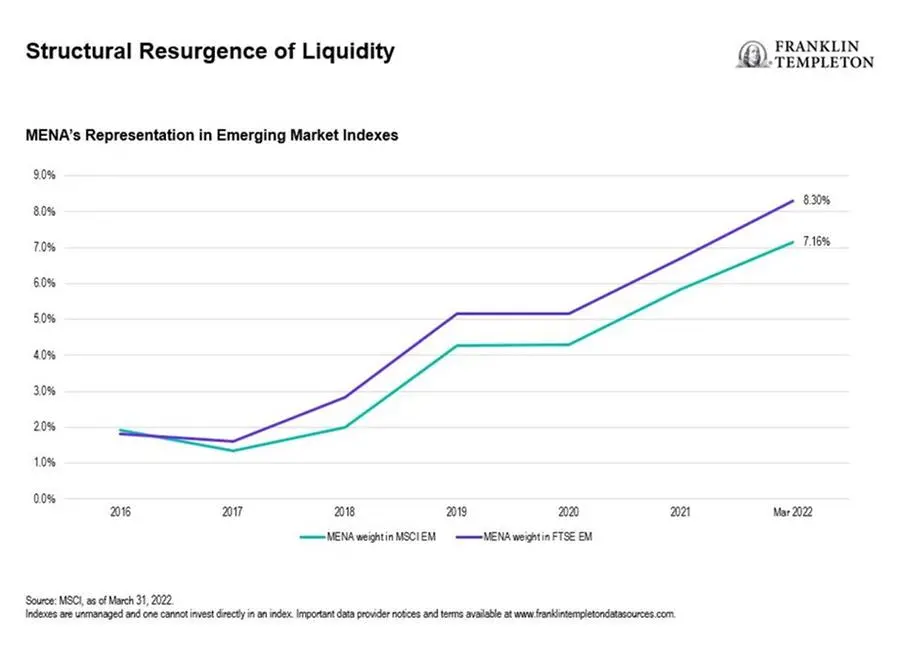

The MENA equity market’s liquidity profile and market share as a percentage of the MSCI Emerging Markets Index has increased significantly over the past few years.4 We have seen substantial increases in asset flows coming into the region since 2021. These flows dramatically increased in March 2022, when many emerging markets investors rotated their allocation out of Russia into the MENA market. GCC initial public offering (IPO) issuances also had a standout year in 2021, and strong post listing performances should continue to provide the needed momentum to push forward more IPOs in the pipeline.

With robust liquidity and high oil prices, equity valuations have been increasing and the region is trading at a premium to emerging markets.5 However, earnings growth has also been above trend since 2021 as MENA economies began to recover from the pandemic. We believe earnings will continue to grow in 2022 and 2023, which should support relatively elevated current valuations. Within the region, there are different valuation levels. Saudi Arabia is the largest market and its valuations have increased the most among its GCC peers due to strong local liquidity, rising optimism and increasing foreign inflows. However, we continue to see dispersion in valuations across GCC markets, which have yet to see similar inflows as Saudi Arabia, despite having similar macroeconomic fundamentals.

Likewise, large-cap stocks in the MENA region have generally performed well since 2016 as liquidity has been focused on that segment of the market.6 However, we believe there is room for mid-cap and small-cap stock performances to improve. It’s usually these stocks that have exposure to parts of the economy outside of oil, and local demand continues to be robust.

Within sectors, higher interest rates have been benefiting the banking sector, which is a large component of the GCC market. On the liability side, especially in Saudi Arabia and the UAE, it is mainly composed of Current Account Savings Accounts (CASA; noninterest-earning deposits). Thus, increases in interest rates should lead to profitability for banks and we think this feature is currently being appreciated by the market.

Despite current geopolitical tensions and interest-rate headwinds, we see a number of opportunities for investors in MENA bond and stock markets. However, not all countries are the same, so we feel having a local presence in the region, with insight into local markets and economies, is paramount.

-Ends-

What Are the Risks?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. Source: Our World in Data, as of April 11, 2022.

2. Source: Bloomberg, as of April 7, 2022.

3. Source: Bloomberg, as of December 31, 2021.

4. Source: MSCI, as of March 31, 2022.

5. Source: Bloomberg, as of close on March 30, 2022.

6. Source: Bloomberg, as of March 31, 2022.