PHOTO

Hong Kong: Fitch Ratings has affirmed the United Arab Emirates' (UAE) Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'AA-' with a Stable Outlook.

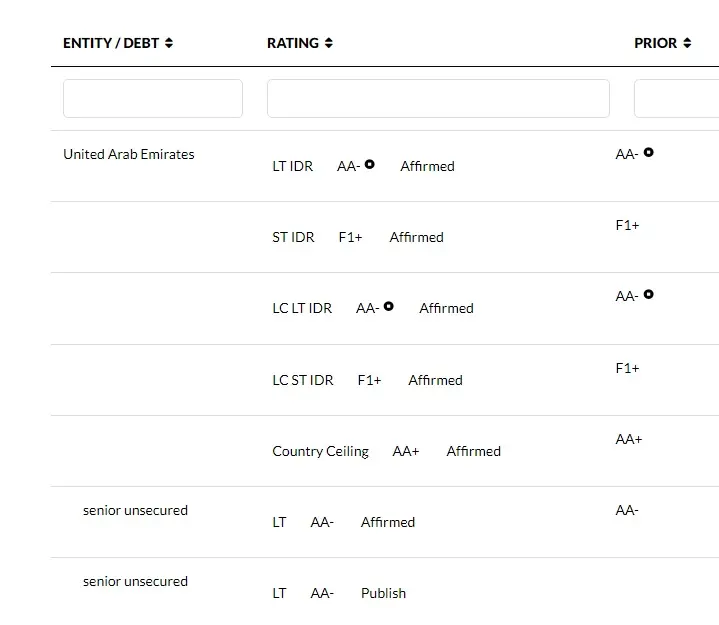

A full list of rating actions is at the end of this rating action commentary.

KEY RATING DRIVERS

Rating Strengths and Weaknesses: The 'AA-' rating reflects the UAE's moderate consolidated public debt level, strong net external asset position and high GDP per capita. This benefits from Abu Dhabi's sovereign net foreign assets (122% of UAE GDP in 2023), which are among the highest of Fitch-rated sovereigns. These strengths are balanced by weak governance indicators relative to rating peers, the UAE's high dependence on hydrocarbon income and the significant leverage of government-related entities (GREs).

The 'AA-' rating applies to the federal government (FG) of the UAE. Fitch evaluates the creditworthiness of the UAE FG based on the consolidated fiscal and external position of all the emirates as is standard practice for federal entities, as well as the FG's standalone fiscal position and institutional set up.

Budget Surpluses: We project the consolidated budget to remain in surplus in 2024 at 4.1% of GDP after 7.8% in 2023, with surpluses in Abu Dhabi (AA/Stable) and Dubai and budget deficits in Ras Al Khaimah (A+/Stable) and Sharjah (not rated).

Fiscal Breakeven Oil Price: We project the UAE fiscal breakeven oil price will average USD64/bbl in 2024-26, although Abu Dhabi GRE dividend plans could be larger than we forecast and reduce this. The consolidated surplus will amount to 3.3% of GDP in 2025 and 2.6% in 2026. Narrower deficits in Sharjah and higher production levels in Abu Dhabi will mitigate the gradual drop in oil prices from USD80 per barrel in 2024 to USD70/bbl in 2025 and USD65/bbl in 2026. We expect fiscal policy to remain pro-cyclical, driven by Abu Dhabi, but less so than pre-pandemic and with a greater share of the impulse delivered by state-owned enterprises (SOE).

Small Federal Government: The FG's budget is small, with revenues and expenditure at about 4% of GDP and its remit is centred around the provision of essential public services such as infrastructure, health, education and police. The FG is required by law to balance its current budget and has a record of broadly balancing the overall budget. Although its revenues and outlays are relatively stable, the FG has limited fiscal flexibility, given its small revenue base and limits on running deficits and issuing debt.

The FG is likely to receive a share of corporate income tax proceeds from 2026, but this is unlikely to materially change its fiscal profile, with a large share of revenue coming from grants from Abu Dhabi and dividends and royalties from federally-owned telecom SOEs, Du and e&.

Moderate Consolidated Government Debt Level: We forecast consolidated UAE government debt at 24% of GDP at end-2024, well below the 'AA' category median of 49%. It will be broadly stable in 2025 and 2026. Individual emirates have varied debt profiles, with Sharjah standing out with a higher debt burden. Dubai repaid AED29 billion (1.5% of UAE GDP) in market and private debt in 2023 and Emirates NBD Bank PJSC's loans to its parent, the Dubai government, fell as well. In an oil price shock scenario, we expect Abu Dhabi would initially choose to increase borrowing over large draw-downs from Abu Dhabi Investment Authority, although the emirate has internal caps on borrowing.

Federal Debt Issuances Continue: The FG's international market debt stands at USD8.5 billion. Proceeds were placed with the Emirates Investment Authority for long-term investment. The debt law could allow proceeds from foreign-currency issuances to be partly used for infrastructure projects, but we expect the authorities not to use this option in case of new issuances.

Local Currency Issuance: The FG started issuing local-currency debt in 2022 and aims to bring the outstanding amount to about AED45 billion over the years, with the objective of building a domestic-currency yield curve rather than funding deficits or projects. The proceeds are invested in highly-rated international government bonds, mostly US Treasuries, with matching maturities. The authorities switched from issuing T-bonds to T-Sukuk during 2023.

High Leverage: Despite a moderate government debt/GDP ratio, Fitch views the UAE as characterised by high leverage in its economy. We estimate overall contingent liabilities from GREs of the emirates and the FG at about 62% of UAE 2023 GDP and gross non-bank private external debt stands at 46% of GDP. Based on publicly available data, a large share of SOE debt is at healthy SOEs with little risk but many do not disclose financial data. The public banking sector's debt was 24% of GDP in 2023. The sector is large with assets of about 200% of GDP in 2023, but risk is limited by the sector's increased net interest margin and strong liquidity.

Close Links with Abu Dhabi: We judge that close political and budgetary links, along with the strong influence of Abu Dhabi over the FG budgeting and the essential nature of public services it provides place the FG higher in Abu Dhabi's support hierarchy than individual emirates, should it be required. However, Abu Dhabi does not provide an explicit guarantee that would ensure unconditional and timely support to the FG.

Non-Oil Growth to Slow: Fitch forecasts overall GDP growth to slow to 3.1% in 2024 and pick up to 4.9% in 2025 after 3.6% in 2023. We expect non-oil growth of 4.3% and hydrocarbon GDP to contract by 0.4% in 2024 as average oil production in 2024 will contract despite the loosening of OPEC+ quotas in 2H24. We project non-oil growth to slow to 3.4% in 2025 but remain relatively robust despite global headwinds, supported by government and GRE spending, a robust real estate sector, dynamic past population growth and GCC demand. The hydrocarbon sector will expand by 9.5% in 2025 due to higher OPEC+ production caps.

Security Risks Remain: In our view, geopolitical remain elevated. Tensions between Iran and Israel and the US are still a risk to the region, in particular to Abu Dhabi's hydrocarbon infrastructure and to Dubai as a trade, tourism and financial hub. Although it has scaled back its military presence, the UAE remains involved in the Yemen civil war, which led to drone attacks in early 2022.

ESG - Governance: The UAE has an ESG Relevance Score (RS) of '5[+]' for both Political Stability and Rights, and for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. These scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model. The UAE has a high WBGI ranking at the 70th percentile, reflecting its record of domestic political stability, strong institutional capacity, effective rule of law and a low level of corruption.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

- Public Finances: A deterioration in Abu Dhabi's sovereign credit profile.

- Public Finances and External Finances: Substantial erosion of the external position of the UAE and/or of individual emirates' fiscal position, for example, due to a sustained period of low oil prices or a materialisation of contingent liabilities.

- Structural Features: A geopolitical shock that negatively affects economic, social or political stability.

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

- Public Finances: Increased confidence that Abu Dhabi would provide unconditional support in the event of need, for example, due to a guarantee for the timely service of the FG debt.

- Structural Features and Macroeconomic Policies: Improvement in structural factors such as a reduction in oil dependence, a strengthening in governance and the economic policy framework, and a reduction in geopolitical risk while maintaining strong fiscal and external balance sheets.

SOVEREIGN RATING MODEL (SRM) AND QUALITATIVE OVERLAY (QO)

Fitch's proprietary SRM assigns the United Arab Emirates a score equivalent to a rating of 'AA-' on the Long-Term Foreign-Currency (LT FC) IDR scale.

Fitch's sovereign rating committee did not adjust the output from the SRM to arrive at the final LT FC IDR.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a LT FC IDR. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

COUNTRY CEILING

The Country Ceiling for the UAE is 'AA+', two notches above the UAE's Long-Term Foreign-Currency IDR. This reflects strong constraints and incentives, relative to the IDR, against capital or exchange controls being imposed that would prevent or significantly impede the private sector from converting local currency into foreign currency and transferring the proceeds to non-resident creditors to service debt payments.

Fitch's Country Ceiling Model produced a starting point uplift of +1 notch above the IDR. Fitch's rating committee applied a further+1 notch qualitative adjustment to this, under the Near-term Macro-Financial Stability Risks and Exchange Rate Risks pillar reflecting that the Country Ceiling Model dips to +1 due to dollarisation of deposits passing 30%. The figure has been historically fairly volatile. It may be related to rising US dollar-denominated hydrocarbon export proceeds or the influx of new residents. External buffers are large and the creation of a UAE dirham yield curve may reduce dollarisation in future. These factors support keeping the Country Ceiling two notches above the IDR.

Sources of Information

The following data limitations were identified and addressed:

a) Standard International Investment Position data for the UAE is not available;

b) there is no disclosure on the size of Abu Dhabi external assets (mostly relating to the Abu Dhabi Investment Authority, ADIA).

a) The main elements of external assets and liabilities are available from emirate sources, creditor sources and the IMF/World Bank/BIS;

b) there is a degree of disclosure on the assets' composition and returns of ADIA and Fitch is provided with some guidance on inflows and outflows. Fitch's estimates of Abu Dhabi's external assets are derived by compounding estimated government cash surpluses using assumptions about returns and asset allocations.

The mitigants above provide us with sufficient confidence in our analysis of the credit profile to maintain or assign the rating.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG CONSIDERATIONS

The UAE has an ESG Relevance Score of '5[+]' for Political Stability and Rights as World Bank Governance Indicators have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and a key rating driver with a high weight. As the UAE has a percentile rank above 50 for the respective Governance Indicator, this has a positive impact on the credit profile.

The UAE has an ESG Relevance Score of '5[+]' for Rule of Law, Institutional & Regulatory Quality and Control of Corruption as World Bank Governance Indicators have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight. As the UAE has a percentile rank above 50 for the respective Governance Indicators, this has a positive impact on the credit profile.

The UAE has an ESG Relevance Score of '4' for Human Rights and Political Freedoms as the Voice and Accountability pillar of the World Bank Governance Indicators is relevant to the rating and a rating driver. As the UAE has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

The UAE has an ESG Relevance Score of '4[+]' for Creditor Rights as willingness to service and repay debt is relevant to the rating and is a rating driver for the UAE, as for all sovereigns. As the UAE has track record of 20+ years without a restructuring of public debt and captured in our SRM variable, this has a positive impact on the credit profile.

The highest level of ESG credit relevance is a score of '3', unless otherwise disclosed in this section. A score of '3' means ESG issues are credit-neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. Fitch's ESG Relevance Scores are not inputs in the rating process; they are an observation on the relevance and materiality of ESG factors in the rating decision. For more information on Fitch's ESG Relevance Scores, visit www.fitchratings.com/topics/esg/products#esg-relevance-scores.

Additional information is available on www.fitchratings.com

PARTICIPATION STATUS

The rated entity (and/or its agents) or, in the case of structured finance, one or more of the transaction parties participated in the rating process except that the following issuer(s), if any, did not participate in the rating process, or provide additional information, beyond the issuer’s available public disclosure.

APPLICABLE CRITERIA

- Sovereign Rating Criteria (pub. 06 Apr 2023) (including rating assumption sensitivity)

- Country Ceiling Criteria (pub. 24 Jul 2023)

APPLICABLE MODELS

Numbers in parentheses accompanying applicable model(s) contain hyperlinks to criteria providing description of model(s).

Country Ceiling Model, v2.0.2 (1)Debt Dynamics Model, v1.3.2 (1)Macro-Prudential Indicator Model, v1.5.0 (1)Sovereign Rating Model, v3.14.1 (1)

ADDITIONAL DISCLOSURES

- Dodd-Frank Rating Information Disclosure Form

- Solicitation Status

- Endorsement Policy

ENDORSEMENT STATUS

| United Arab Emirates | EU Endorsed, UK Endorsed |

DISCLAIMER & DISCLOSURES

All Fitch Ratings (Fitch) credit ratings are subject to certain limitations and disclaimers. Please read these limitations and disclaimers by following this link: https://www.fitchratings.com/understandingcreditratings. In addition, the following https://www.fitchratings.com/rating-definitions-document details Fitch's rating definitions for each rating s

READ MORE

SOLICITATION STATUS

The ratings above were solicited and assigned or maintained by Fitch at the request of the rated entity/issuer or a related third party. Any exceptions follow below.

ENDORSEMENT POLICY

Fitch’s international credit ratings produced outside the EU or the UK, as the case may be, are endorsed for use by regulated entities within the EU or the UK, respectively, for regulatory purposes, pursuant to the terms of the EU CRA Regulation or the UK Credit Rating Agencies (Amendment etc.) (EU Exit) Regulations 2019, as the case may be. Fitch’s approach to endorsement in the EU and the UK can be found on Fitch’s Regulatory Affairs page on Fitch’s website. The endorsement status of international credit ratings is provided within the entity summary page for each rated entity and in the transaction detail pages for structured finance transactions on the Fitch website. These disclosures are updated on a daily basis.

Peter Fitzpatrick

Senior Director, Corporate Communications

Fitch Ratings

30 North Colonnade

London E14 5GN