Funding risk is a prominent topic among investors in GCC banks, particularly during the transition from cheap and abundant liquidity to a more restrictive environment. Major central banks have also made it clear that interest rates will be higher for longer, meaning liquidity will be scarcer and more expensive. This could affect banking systems in emerging markets with significant or growing external debt position such as Bahrain.

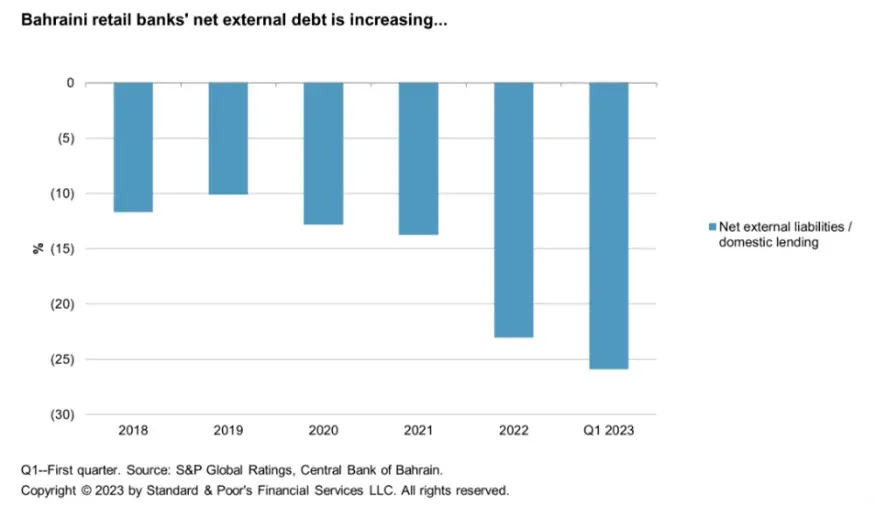

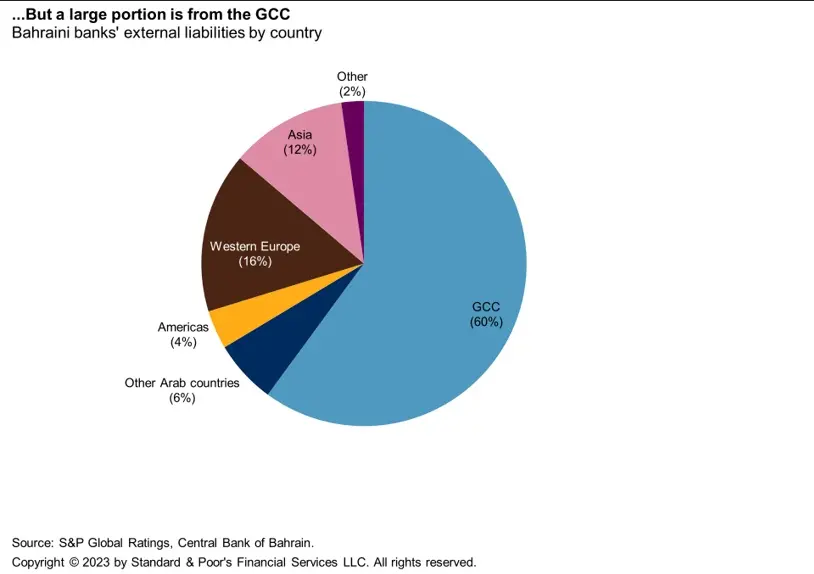

Bahrain's retail banks (onshore banks) have large and expanding net external liabilities. On 31 March, 2023, they reached 26% of total domestic lending (see Chart 1). However, S&P Global Ratings notes that 60% of the foreign liabilities are interbank, and 60% are sourced from the GCC (see Chart 2). Given the ownership structures of some Bahraini retail banks, the Credit Ratings agency assume that a portion of this external funding is from foreign parents. S&P Global Ratings also assumes that external funding will remain stable under its base-case scenario.

Chart 1:

Chart 2:

Dr. Mohamed Damak, Senior Director and Head of Islamic Finance, S&P Global Ratings commented: “Bahraini retail banks' loan to deposit ratios have been consistently below 80% for the past five years. Therefore, in our view, a portion of local deposits and external liabilities are recycled into government and local central bank exposures. On 31 March, 2023, these exposures represented almost one-quarter of retail banks' balance sheets.

“The other peculiarity of the Bahraini banking system stems from the large wholesale sector. However, we see the risk of disruption to retail banks as relatively limited. Wholesale banks' domestic activity represented about 15% of total assets and remained stable over the past few years. On 31 March, 2023, about half of this exposure comprised interbank transactions-wholesale banks' lending to local retail or wholesale banks--and another one-quarter was direct lending to the Bahraini private sector. Exposure to the government represented about 15% of total local assets at the same date. Furthermore, about 78% of these exposures were financed using local sources, meaning that the overall domestic net contribution from wholesale banks to the local economy stood at $4.2 billion, or about 4% of the retail banking system's size.”

The availability of a well-functioning domestic debt capital market can make a difference for Bahrain’s banking sector's funding opportunities. In terms of relative stability, funding sourced from the domestic debt capital market tends to be more stable than cross-border funds, but less stable than core customer deposits. Having a broad and deep local debt capital market can therefore help the banking system reduce its dependence on external funding and ease concentration and maturity mismatches.

About S&P Global Ratings

S&P Global Ratings is the world's leading provider of independent credit ratings. Our ratings are essential to driving growth, providing transparency and helping educate market participants so they can make decisions with confidence. We have more than 1 million credit ratings outstanding on government, corporate, financial sector and structured finance entities and securities. We offer an independent view of the market built on a unique combination of broad perspective and local insight. We provide our opinions and research about relative credit risk; market participants gain independent information to help support the growth of transparent, liquid debt markets worldwide.

S&P Global Ratings is a division of S&P Global (NYSE: SPGI), which provides essential intelligence for individuals, companies and governments to make decisions with confidence. For more information, visit www.spglobal.com/ratings.

Media contacts: Tally Sargent, Hanover Communication