(Geneva) - The International Air Transport Association (IATA) announced that the recovery in air travel continued in November 2021, prior to the emergence of Omicron. International demand sustained its steady upward trend as more markets reopened. Domestic traffic, however, weakened, largely owing to strengthened travel restrictions in China.

Because comparisons between 2021 and 2020 monthly results are distorted by the extraordinary impact of COVID-19, unless otherwise noted all comparisons are to November 2019, which followed a normal demand pattern.

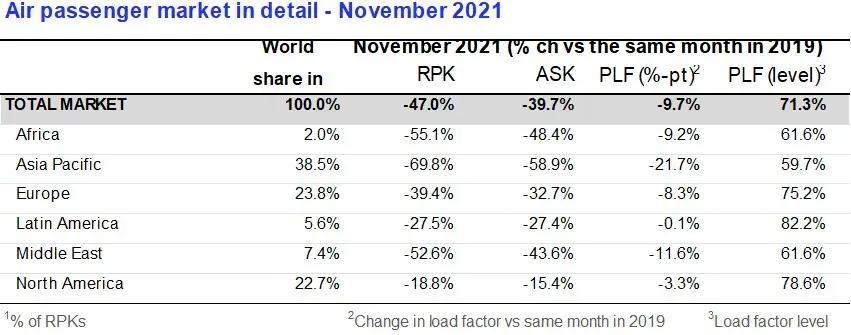

- Total demand for air travel in November 2021 (measured in revenue passenger-kilometers or RPKs) was down 47.0% compared to November 2019. This marked an uptick compared to October’s 48.9% contraction from October 2019.

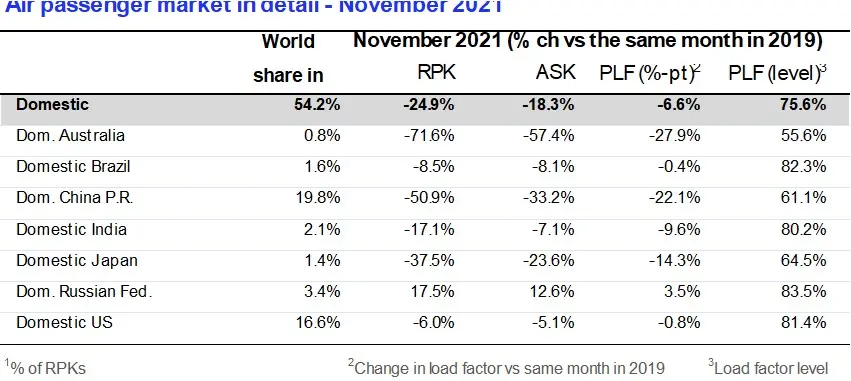

- Domestic air travel deteriorated slightly in November after two consecutive monthly improvements. Domestic RPKs fell by 24.9% versus 2019 compared with a 21.3% decline in October. Primarily this was driven by China, where traffic fell 50.9% compared to 2019, after several cities introduced stricter travel restrictions to contain (pre-Omicron) COVID outbreaks.

- International passenger demand in November was 60.5% below November 2019, bettering the 64.8% decline recorded in October.

“The recovery in air traffic continued in November. Unfortunately, governments over-reacted to the emergence of the Omicron variant at the close of the month and resorted to the tried-and-failed methods of border closures, excessive testing of travelers and quarantine to slow the spread. Not surprisingly, international ticket sales made in December and early January fell sharply compared to 2019, suggesting a more difficult first quarter than had been expected. If the experience of the last 22 months has shown anything, it is that there is little to no correlation between the introduction of travel restrictions and preventing transmission of the virus across borders. And these measures place a heavy burden on lives and livelihoods. If experience is the best teacher, let us hope that governments pay more attention as we begin the New Year, ” said Willie Walsh, IATA’s Director General.

International Passenger Markets

European carriers’ November international traffic declined 43.7% versus November 2019, much improved compared to the 49.4%% decrease in October versus the same month in 2019. Capacity dropped 36.3% and load factor fell 9.7 percentage points to 74.3%.

Asia-Pacific airlines saw their November international traffic fall 89.5% compared to November 2019, slightly improved from the 92.0% drop registered in October 2021 versus October 2019. Capacity dropped 80.0% and the load factor was down 37.8 percentage points to 42.2%, the lowest among regions.

Middle Eastern airlines had a 54.4% demand drop in November compared to November 2019, well up compared to the 60.9% decrease in October, versus the same month in 2019. Capacity declined 45.5%, and load factor slipped 11.9 percentage points to 61.3%.

North American carriers experienced a 44.8% traffic drop in November versus the 2019 period, significantly improved over the 56.7% decline in October compared to October 2019. Capacity dropped 35.6%, and load factor fell 11.6 percentage points to 69.6%.

Latin American airlines saw a 47.2% drop in November traffic, compared to the same month in 2019, a marked upturn over the 54.6% decline in October compared to October 2019. November capacity fell 46.6% and load factor dropped 0.9 percentage points to 81.3%, which was the highest load factor among the regions for the 14th consecutive month.

African airlines’ traffic fell 56.8% in November versus two years’ ago, improved over the 59.8% decline in October compared to October 2019. November capacity was down 49.6% and load factor declined 10.1 percentage points to 60.3%.

Domestic Passenger Markets

Australia remained at the bottom of the domestic RPK chart for the fifth consecutive month with RPKs 71.6% below 2019, albeit this was improved from a 78.5% decline in October, owing to the reopening of some internal borders.

US domestic traffic was down just 6.0% compared November 2019 – improved from an 11.1% fall in October, thanks in part to strong Thanksgiving holiday traffic.

View the full November Air Passenger Market Analysis

-Ends-

For more information, please contact:

Corporate Communications

Tel: +41 22 770 2967

Email: corpcomms@iata.org

- IATA (International Air Transport Association) represents some 290 airlines comprising 83% of global air traffic.

- You can follow us at https://twitter.com/iata for announcements, policy positions, and other useful industry information.

- Statistics compiled by IATA Economics using direct airline reporting complemented by estimates, including the use of FlightRadar24 data provided under license.

- All figures are provisional and represent total reporting at time of publication plus estimates for missing data. Historic figures are subject to revision.

- Domestic RPKs accounted for about 54.3% of the total market.

- Explanation of measurement terms:

- RPK: Revenue Passenger Kilometers measures actual passenger traffic

- ASK: Available Seat Kilometers measures available passenger capacity

- PLF: Passenger Load Factor is % of ASKs used.

- IATA statistics cover international and domestic scheduled air traffic for IATA member and non-member airlines.

- In 2020, total passenger traffic market shares by region of carriers in terms of RPK were: Asia-Pacific 38.6%, Europe 23.7%, North America 22.7%, Middle East 7.4%, Latin America 5.7%, and Africa 1.9%.

© Press Release 2022

Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.