PHOTO

Ras Al Khaimah, United Arab Emirates – The National Bank of Ras Al Khaimah (RAKBANK) today reported its financial results for the first Half of 2024.

| Highlights | Total Income AED 2.3B +8.7% YoY | Total Assets AED 80.4B +11.9% YoY | Deposits AED 58.5B YoY | Return on Equity YTD | Return on Assets 2.9% YTD |

Key Financial Highlights – H1 2024

RAKBANK delivers record net profit after tax of AED 1.1B, growth of 21% YoY, driven by diversified growth in balance sheet, continued sales momentum and strong credit quality.

- Income up 8.7% YoY, supported by a net interest margin of 4.6%, on the back of well diversified asset growth and sticky CASA base, augmented by higher Foreign Exchange & Investment income.

- Operating Expenditure was at AED 789M, reflecting a growth of 3% YoY, as the Bank continues to grow the business and invest in technology and talent on a sustainable basis.

- Gross loans & advances at AED 43.7B up 9.4% YoY, driven by growth across all segments, with Wholesale Banking loans and advances growing by 19.4%, in line with the Bank’s diversification strategy.

- Customer deposits at AED 58.5B up 19.4% YoY, with a CASA ratio of 61.6%.

- Portfolio credit quality remains robust with cost of risk at 1.7% v/s 2.6% in H1’23, supported by benign credit environment and shift in business mix towards secured low risk assets.

- Total provisions coverage on gross loans & advances is at 6.1% compared to 5.7% in H1’23.

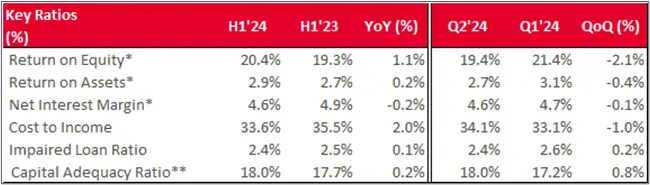

- Shareholder returns remain strong with Return on Equity (ROE) of 20.4% and Return on Assets (ROA) of 2.9%.

- The Bank remains liquid and well capitalised with Capital Adequacy Ratio (CAR) at 18.0% vs. 17.8% as at 31st December 2023.

- Strong liquidity position as reflected by an Eligible Liquid Asset Ratio of 15.5% and Advances to Stable Resources Ratio at 79.4%

- The impaired loan ratio improved to 2.4% against 2.6% as at 31st December 2023.

Key Financial Highlights – Q2 2024

- Operating Income for Q2’24 was at AED 1,174M, reflecting an increase of 6.6% YoY.

- Profit before tax for Q2’24 was at AED 566M, reflecting an increase of 25.6% YoY.

- Gross loans & advances for the quarter are up 1.1% vs Q1’24 driven by growth across all the segments, with Mortgage loans surpassing the AED 10B mark.

- Customer Deposits reflected a growth of 5.6% vs Q1’24, driven by growth in both time & CASA deposits.

Raheel Ahmed, Group CEO:

"Our strategic transformation remains on course, and we are making strong progress on becoming the ‘digital bank with a human touch’. The progress of our transformation is evidenced in our record-breaking financial performance in H1 2024. We continue to diversify our balance sheet, reduce our risk profile, and add on new innovative products and services for our customers. The Bank remains well capitalised and delivers strong shareholder returns.

We've made significant strides in enhancing accessibility for our customers anytime, anywhere. Our customers logged into our digital banking platforms 24 million times in H1 2024 (up 13% YoY). In Personal Banking, 98% of financial transactions were conducted digitally. Since the launch of our digital onboarding journeys, 83% of Personal Banking accounts are now opened digitally, and 49% of new bank cards are initiated through this digital onboarding. What I'm particularly pleased about is the progress in our cultural transformation, empowering our colleagues to take ownership of delivering an awesome customer experience.

I am delighted to announce that as part of our commitment to ESG, RAKBANK has become the first bank in the region to issue a Social Bond. This is a key milestone for RAKBANK as it reinforces our commitment to supporting SMEs and the UAE’s economy. In line with our Social Finance Framework, the proceeds of the bond will be utilised to support the healthcare industry and provide loans to Micro, Small & Medium Enterprises, in line with “We the UAE 2031” vision.

As we enter the second half of 2024, we remain watchful of the geo-political dynamics shaped by elections affecting 72% of the world’s population, ongoing military conflicts, and economic indicators in major economies like the USA and China. However, the UAE economy remains resilient on the back of oil prices, real estate, trade and tourism. We approach the second half of 2024 with confidence as we remain committed to building on the Bank’s strengths and delivering on our strategy. "

| Digital Transactions +12% YoY | Card Spends

| Payment through our rails (In/Out) | Digitally Active Customers +14% YoY |

Financial Highlights for Q2/H1 2024

Figures in brackets represent unfavorable movements

* Annualized

**After application of Prudential Filter

Numbers may not add up due to rounding

Profitability growth supported by Income momentum (H1’24)

- 33% increase in Profit before tax to AED 1.2B in H1 2024. Net Profit before tax for the quarter at AED 565.9M, up 25.6% compared to Q2 2023.

- Net Interest Income and Income from Islamic products net of distribution to depositors was AED 1.8B.

- Interest income from conventional loans and investments was up by 19.4% compared to H1 2023, while interest costs on conventional deposits and borrowings was up by 41%. Net income from Sharia-compliant financing was lower by 13.2%.

- Non-interest Income was up by AED 44.1M, mainly due to an increase of AED 27.5M in Investment income, AED 18.5M in Foreign exchange and AED 39.3M in Other Income. This was offset by higher net insurance expense by AED 14.5M.

- Operating Income was up by AED 188.6M, mainly due to increase in Net Interest Income by AED 144.6M and Non-interest income by AED 44.1M.

- Operating expenses at AED 788.8M for H1 2024, reflected an increase of 2.8% as compared to H1 2023 and 2.0% compared to Q2 2023, as the Bank continued to invest for growth. Compared to the previous quarter, the expenses are higher by 3.1%.

- The Operating Expenses for first half of the year were higher mainly due to an increase of AED 36.8M in staff costs, AED 29.1M in information and technology expenses, depreciation by AED 4.9M, marketing expenses by AED 3.3M offset by lower card and other expenses 55M.

- Cost to Income Ratio for the Bank decreased to 33.6% compared to 35.5% at the end of the same period last year and 36.4% for FY 2023.

- Provisions for credit loss at 364.2M for H1 2024, lower by 25.9% compared to H1 2023 and higher by 32.6% compared to Q1 2024.

- Net credit losses to average loans and advances closed at 1.7% compared to 2.6% at the end of the first half of 2023.

- Group Profit after tax was at AED 1.1B, up 21% compared to H1 2023.

Total Balance Sheet at AED 80.4 billion, with a strong uptick across customer segments

- Balance sheet crosses AED 80.0B as the Total Assets increased by AED 8.5B YoY reflecting a growth of 11.9%, with an increase in Gross Loans and Advances by AED 3.8B, Investments by AED 2.2B, Cash and Balance with CBUAE by AED 1.4B and due from other banks by AED 1.4B YoY.

- Customer advances in Wholesale Banking increased by AED 715M, Business Banking segment by AED 538M and Retail Banking segment by AED 423M, compared to 31st December 2023. Strong balance sheet momentum was visible across all the segments.

- Wholesale Banking segment reflects a strong YTD growth of 6.0%, mainly driven by corporate loans, as we strategically diversify our portfolio mix.

- Growth in Retail Banking was supported by a strong sales momentum across products with mortgage loans reflecting 8.6% YTD growth, Credit Cards growing by 2.3% and Auto Loans by 1.1%.

- Business Banking segment recorded 5.5% growth YTD backed by 7.7% growth in SME Loans, and RAKbusiness Loans growing by 2%.

- Customer Deposits increased by 19.4% against the first half of 2023 and 16.0% YTD, AED 8B, mainly driven by an increase of AED 5.8B in time deposits and AED 2.3B in CASA accounts with a CASA ratio of 61.6%, endorsing the trust our customers place in the RAKBANK franchise and our services.

Capital and Liquidity

- Capital adequacy ratio for the Bank was at 18.0% against 17.8% as at Dec’23.

- Eligible Liquid Assets Ratio for the Bank was at 15.5% against 13.0% as at Dec’23 while Advances to Stable Resources Ratio was 79.4% against 82.1% as at Dec’23.

Cash Flows

- Cash and cash equivalents as at 30th June 2024 were at AED 9.5B increasing by AED 1.6B against Dec’23.

- Net cash generated from operating activities was AED 3.7B, AED 0.8B was used in investing activities and AED 1.4B was used in financing activities.

Impact of Capital Expenditure and Developments

- The capital expenditure for the half year ended 30th June 24 amounted to AED 65.9M compared to AED 80.3M in H1 2023, as the Bank continues to grow the business and invest in technology and talent on a sustainable basis.

Ratings

RAKBANK is rated by leading rating agencies. The current ratings are summarised below. These ratings reflect the institutional strength of the Bank that is backed by trust and transparency in financial reporting and disclosures.

| Rating Agency | Last Update | Deposits | Outlook | |

| Moody’s | April 2024 | Baa1 / P-2 | Stable | |

| Fitch | March 2024 | BBB+ / F2 | Stable | |

| Capital Intelligence | August 2023 | A / A1 | Stable | |

-Ends-

About RAKBANK

RAKBANK, also known as the National Bank of Ras Al Khaimah (P.S.C), is one of the UAE's oldest yet most dynamic banks. Since 1976, RAKBANK has been a market leader, offering a wide range of banking services across the UAE.

We’re a public joint stock company based in Ras Al Khaimah, UAE, with our head office located in the RAKBANK Building on Sheikh Mohammed Bin Zayed Road. The Government of Ras Al Khaimah holds the majority of our shares, which are publicly traded on the Abu Dhabi Securities Exchange (ADX).

RAKBANK stands out for its innovation and unwavering commitment to delivering awesome customer experiences. Our transformative digital journey aims to be a 'digital bank with a human touch,' accompanying you during key moments.

With 21 branches and advanced Digital Banking solutions, we offer a wide range of Personal, Wholesale, and Business Banking services. Through our Islamic Banking unit, RAKislamic, we provide Sharia-compliant services to make your banking experience seamless, whether you visit us in person or online.

For more information, please visit www.rakbank.ae or contact the Call Centre on +9714 213 0000.

Alternatively, you can connect with us on our social media platforms:

twitter.com/rakbanklive

Instagram.com/rakbank

tiktok.com/@rakbank

linkedin.com/rakbank

For enquiries, please contact:

Michelle Saddi

michelle.saddi@rakbank.ae

DISCLAIMER

The information in this document has been prepared by The National Bank of Ras Al Khaimah (P.S.C) a public joint stock company, United Arab Emirates (“RAKBANK”) and is general background information about RAKBANK’s activities and is not intended to be current as on the date of the document. This information is given in summary form and does not purport to be complete.

The information is intended to be read by investors having knowledge in investment matters. Information in this document, including forecast or financial information, should not be considered as an advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling securities or other financial products or instruments and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial and legal advice. All securities and financial product or instrument transactions involve risks, which include (among others) the risk of adverse or unanticipated market, financial or political developments and, in international transactions, currency risk.

This document may contain published financial information, or information obtained from sources believed to be reliable, forward-looking statements based on numbers or estimates or assumption that are subject to change including statements regarding our intent, belief or current expectations with respect to RAKBANK’s businesses and operations, market conditions, results of operation and financial condition, specific provisions and risk management practices. Readers are cautioned not to place undue reliance on these forward-looking statements. RAKBANK does not undertake any obligation to publicly release the result of any revisions to these forward-looking statements to reflect events or circumstances after the date hereof to reflect the occurrence of unanticipated events. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside RAKBANK’s control. Past performance is not a reliable indication of future performance.

RAKBANK disclaims any responsibility for the accuracy, fairness, completeness and correctness of information contained in this document including forward looking statements and to update or revise any information or forward-looking statement to reflect any change in RAKBANK’s financial condition, status or affairs or any change in the events, conditions or circumstances on which a statement is based. Neither RAKBANK nor its related bodies, corporate, directors, employees, agents, nor any other person, accepts any liability, including, without limitation, any liability arising from fault or negligence, for any direct, indirect or consequential loss arising from the use/reference of this document or its contents or otherwise arising in connection with it for the quality, accuracy, timeliness, continued availability or completeness of any data or calculations contained and/or referred to in this document.