PHOTO

Main Highlights

- Net Profit at record EGP 6,060 million, up 59% Year-on-Year;

- Customer Deposits reached EGP 84 billion, up 4% Year-on-Year;

- Gross Loans reached EGP 51.9 billion, up 35% Year-on-Year;

- Current and Saving Accounts to Total Deposits reached 58% up by 4% Year-on-Year;

- Non-Performing Loans ratio at 2.4% and Coverage Ratio at 181.3%;

- Loans-to-Deposit Ratio at 62%, up +14% Year-on-Year driven by robust loan growth;

- Resilient Capital Structure, Capital Adequacy Ratio of 20.05%;

- Return on Average Assets at 7.3% up 1.5% Year-on-Year and Return on Average Equity at 47.4% up 3.4% Year-on-Year;

Economic Dynamics:

The global economy continues to demonstrate resilient growth in 2024 supported by falling inflation and above expectation levels of employment and consumption. This has triggered reversal of tighter monetary policy conditions by major central banks in developed economies with a close monitoring of upside risk elements on inflation driven by accelerating trade and geo-political tensions.

Domestically, post the positive events in Q1 2024, the economy is gradually recovering despite a very marginal uptick in inflation in Q3 2024 driven by fiscal measures (fuel, energy and electricity price hikes) and the related impact on prices of key items of consumption. The possibility of escalation in the regional geopolitical risks continues to be a key risk indicator for the economy in the coming quarters.

Crédit Agricole Egypt: Robust performance despite challenging environment

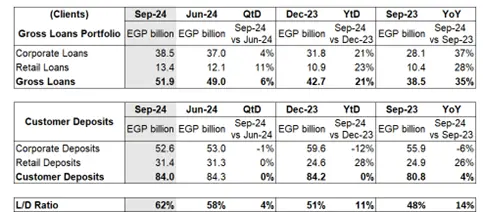

Crédit Agricole Egypt (CAE) continued to maintain its solid performance through 9M 2024, generating a Net Banking Income of EGP 10,332 million, up 49%YoY, on the back of good performance by all business lines. Gross Loans outstanding reaching EGP 51.9 billion, up 35%YoY and Customer Deposits reaching EGP 84billion, up 4%YoY.

Corporate banking continued to achieve remarkable results in 9M 2024, despite the evolving market conditions in 9M 2024. The lending portfolio had good growth of EGP 10.4billion, thereby achieving 37% YoY growth, with resilient and high quality of assets. The corporate deposits were lower by EGP 3.3billion, -6% YoY driven mainly by LCY utilization for clearance of trade backlogs post devaluation in Mar 24 plus calibration of liability profile in response to competitive pricing. The strong performance reflects CAE’s commitment to providing best-in-class financial solutions and services to our corporate clients. Corporate performance improved significantly driven by strategic focus on product diversification and boosting of non-interest income.

Retail banking achieved good portfolio growth in 9M 2024 i.e. +28% for Loans and +26% for Deposits YoY. The performance was driven by targeted marketing campaigns, launching of new products and client acquisition despite the competitive CD market during 9M 2024. Cash loans production achieved growth of +23% YoY driven by strategic cross-sell initiatives. Auto loans production achieved robust growth of +131% YoY driven by higher ticket size while market continued to being short of supply. Mortgage loans production was higher by 12% YoY supported by CBE initiatives and targeted campaigns.

The bank witnessed growth in active customer i.e. 3% QoQ sequentially and 8% YoY driven by campaign/offers directed to customer acquisition, customer re-activation, loan campaigns and cross-sell. This was also supported by launching new products i.e. AHLAN current account for non-digital acquisition, AHLAN digital account for digital acquisition, Excellence account for private banking customers, Cash Loan Program (Drive cash), Education Loans, Solar Loans, New Visa Platinum Business Cards, 3 new floating CDs (Excellence, Premium & Standard) to meet all our clients’ needs, and participation in events hosted by Clubs/Universities and Closed Communities.

Dynamic Commercial Activity and Solid Balance Sheet Structure

Commercial activity evolution continues to be good and at anticipated levels with limited impact due to the evolution of the CDs and FX market thereby providing both Corporate and Individual customers with adequate financial solutions and increasing the active customer base. Gross Loans portfolio (including Loans to Banks) increased 21% YTD, to reach EGP 51.9billion, while Customer Deposits almost remained stagnant YTD, to reach EGP 84billion.

*Corporate and Retail breakdown based on Published Financial Statements

**Nil Loans to banks for all mentioned periods

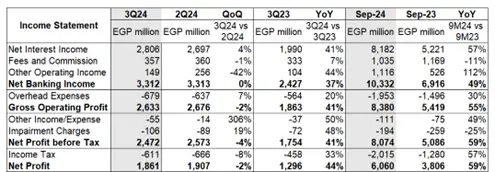

Profitability Performance

Net Banking Income (NBI) increased +49% YoY, reaching EGP 10,332 million, where Net Interest Income increased +57% YoY due to higher yields, supported by exceptional other income +112% driven by FX activities. Operating Expenses increased +30% YoY demonstrating efficient controls on costs despite higher inflation and EGP devaluation of ~56% in 9M 2024. Cost to Income Ratio (C/I) reduced to 18.9% from 21.6% and Gross Operating Income (GOI) increased +55% YoY to reach EGP 8,380 million.

Lower cost of risk at EGP -194 million, compared to -259 million in the same period last year driven by resilient portfolio and strong recoveries demonstrating the bank’s prudent risk management framework.

Net Profit reached EGP 6,060 million, +59% YoY, driven by higher NBI with effective control on operating expenses complemented by prudent risk management.

QoQ sequentially, NBI remained stagnant and GOI decreased by-2% mainly resulting from slower commercial activity growth in Q3 2024 and marginal uptick in the operating expenses during the quarter driven by inflation.

* Income Statement based on managerial reporting

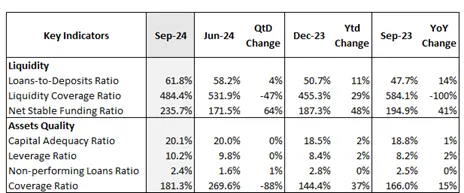

High Quality of Assets, Strong Solvency and Liquidity

CAE NPL ratio at 2.4% in Q3 2024 and continues to remain among one of the lowest ratios within the banking sector and complemented by strong coverage buffer, demonstrating the high quality credit positioning of the bank to pursue healthy lending portfolio growth, with prudent risk management practices in place.

Furthermore, the bank’s strong liquidity position and solid capital buffer, well above regulatory requirements, provide adequate safeguard to absorb shocks, if any.

* CAR, LCR, NSFR and Leverage as reported to CBE.

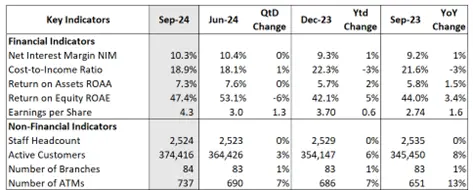

Key Financial and Business Indicators

*Net Interest Margin “NIM” based on managerial reporting and Earnings per Share net of Profit Share to Employees

Digital Development

CAE digital channels continue to show competitive positive achievements.

For retail, banki Mobile continues to be an essential tool for reinforcing CAE position as one of the leading banks in digital banking with more than 3.1M login during Q3 2024. CAE digital channels have witnessed more than 3.4M transactions executed during Q3 2024 (+195% YoY) with a remarkable 99% of domestic transfers being done online.

CAE went live on INSTAPAY in May 2023 and continues to make significant contribution i.e. over 8.4M outgoing transactions thereby demonstrating the participation of the bank within the growing digital banking ecosystem in alignment with the continuous efforts of the Central Bank of Egypt.

For corporate and SMEs customers, 40% of the companies have been digitally active on the online platform, with almost half of the domestic transfers now done digitally with 28% increase over Q3 2023. CAE witnessed an increase in digital governmental payments volumes by around 160% in Q3 2024 vis-à-vis Q3 2023.

For Ecommerce, CAE continued to capitalize on the payment acceptance product "banki Commerce" contributing further towards the Central Bank efforts for a "less cash society" as well as the gradual shift to payment acceptance. As of 9M24, "banki Commerce" witnessed 22K transactions vis-à-vis 3.2K transactions for 9M23 i.e. increase of 7X transactions processed through the new gateway since inception. CAE remains committed to its ambitious vision in the Payment Acceptance field, and its unique onboarding journey continues to make it easy for all customers.

Sustainability and CSR Activities

As a step forward in its ambition to promote green and clean finance, the bank has signed facility agreement with European Bank for Reconstruction and Development (EBRD) under the Green Energy Finance Facility (GEFF) and Global Climate Fund (GCF) program to support its SMEs and other eligible clients. The bank is already promoting sustainable financing solutions to its individual clients with the launch of solar loan campaign in H2 2023.

Credit Agricole Egypt has published its third integrated sustainability report in Q3 2024, titled "Embracing an elevated journey". The report reflects CAE's strategic direction, towards adding value for its customers, investors, the general public, and the economy it serves. The bank is the first and only one in Egypt to introduce integrated reporting in alignment with Integrated Reporting (IR) framework and in compliance with the Global Reporting Initiative (GRI).

CAE Foundation and its partner Education First held the annual graduation ceremony of Y2024 of EBHAR MISR Program for Talented Youth. The event celebrates the new class of students that join the program and graduate after attending a two-week boot camp. EBHAR MISR Program adopts young students who are talented in the fields of art, science and technology. With an average of 20 students joining every year, the program alumnae now consists of 120 students who continue to undergo skill-development training in their respective field.

About Credit Agricole Egypt

CAE is the sole French Bank in Egypt established in 2006 and is listed in the Egyptian Stock Exchange since 2015. CAE has one subsidiary Egyptian Housing Finance Company (EHFC) with 99.99% percent stake.

Credit Agricole Egypt continues to leverage on its digital infrastructure, diversified expertise, solid balance sheet structure, prudent risk management, strong liquidity position and adequate capital buffer allowing the bank to pursue its strategic profitable growth by serving its customers as well as the economy.