Sustained profits growth

- US$ 410 million of net profits in 9M-18, increasing by 20% over the same period of 2017

- US$ 132 million of net profits generated from entities abroad, representing 32% of total profits

- 8% cost to income ratio in 9M-18, compared to 51.4% in the same period of 2017

- 4% of return on average common equity, improving from 13.4% in 2017

Key balance sheet metrics

- US$ 45.7 billion of consolidated assets

- US$ 30.9 billion of consolidated customers' deposits

- US$ 13.7 billion of consolidated net loans

- US$ 3.1 billion of common shareholders' equity and US$ 3.8 billion of total shareholders' equity

Reinforced financial standing

- 4% of CET1 ratio and 18.2% of total capital adequacy ratio

- 4% of primary liquidity to customers' deposits ratio

- 5% of gross doubtful loans to gross loans ratio,

- 107% coverage of doubtful loans by specific provisions and real guarantees

Further deceleration in growth in Lebanon amid an US$ 4.6 billion increase in deposits

The Lebanese economy is growing by an estimated 2% this year as per the Central Bank of Lebanon versus 2.5% last year, with the deceleration related mostly to dampened investor appetite ahead of the awaited government formation post the May 2018 parliamentary elections. Banking deposits reported an increase of US$ 4.6 billion year-to-August, rising on an annualised basis by 4.2% amid stable loans to the private sector.

Mild rebound in economic growth in the MENA, within a 5% GDP growth in Egypt and economic rebalancing in Turkey

- In the MENA region, on-going reforms and higher oil prices have helped to offset the impact of the hike in interest rates and adverse economic environment resulting in a mild rebound in economic growth this year to circa 2%.

- In Egypt, all indicators point to a bullish cycle, with growth being revised upwards by the IMF to above 5% for 2018, among the highest in the Middle East and North Africa region, while banking sector deposits grew by 19% in US$ term over the year-ending July 2018.

- In Turkey, the economy, which went this year into its worst currency devaluation since 2001 driving inflation to a record 25% level in September, is starting to rebalance, with less output growth amid higher rates, but with noticeably better external imbalances post devaluation, which could provide the much-needed support to the financial/monetary outlook looking forward.

Consolidated assets grew by 4.5% in nominal terms as compared to 2.6% for MENA banks

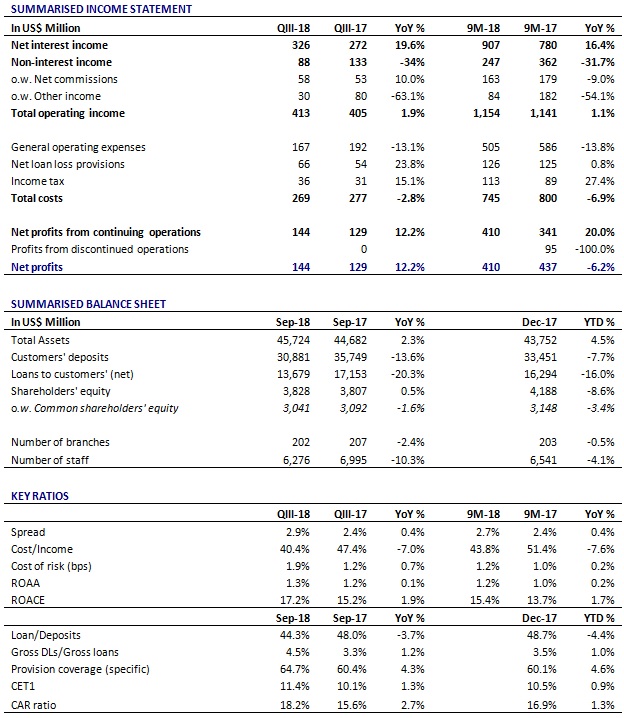

Consolidated assets rose by US$ 2 billion in the first nine months of 2018 reaching US$ 45.7 billion at end-September 2018. This corresponds to a growth of 4.5%, as compared to 2.6% on average for banks in the MENA region. At constant exchange rate (same rate as at end-December 2017), assets would have increased by US$ 3.7 billion in real terms, or 8.4%. Total assets under management, comprising of fiduciary deposits, custody accounts and assets under management, reached US$ 13.1 billion at the same date. Accordingly, total assets and assets under management reaches US$ 58.8 billion. The size of Bank Audi makes it the only Lebanese bank to be ranked among the top 20 Arab banking groups.

Deposits in Audi Lebanon increased by US$ 450 million

Consolidated customers’ deposits amounted to US$ 30.9 billion at end-September 2018, registering a contraction relative to end-December 2017 by US$ 2.6 billion, of which US$ 1.7 billion of real decrease and circa US$ 1 billion of FX translation impact. Still deposits of Bank Audi Lebanon increased by US$ 450 million over the same period as deposits denominated in Lebanese Pounds rose by US$ 934 million with some customers opting to convert their USD deposits to benefit from the LBP rates.

Loans decrease due to settlements and loan reduction in exposures in Turkey

Consolidated loans stood at US$ 13.7 billion as at end-September 2018 as compared to US$ 16.3 billion as at end-December 2017. This is equivalent to a contraction by US$ 2.6 billion, of which US$ 1 billion due to FX translation impact. The remaining decrease represents loan settlements and reduction of loan exposures particularly in Odea Bank amid an adverse environment.

Asset quality

Consolidated gross doubtful loans reached US$ 647 million as at end-September 2018 as compared to US$ 600 million as at end-December 2017. In parallel, gross doubtful loans represented 4.5% of gross loans as at end-September 2018 as compared to 3.5% as at end-December 2017. This movement is mostly attributed to the 16.4% contraction in gross loans. Coverage ratio of doubtful loans by specific provisions increased to 64.7% and reaches 107% when including real guarantees. In addition, collective provisions amounted to US$ 200 million, representing 1.5% of net loans.

Improved financial flexibility

The Bank’s core equity tier one ratio (CET1) as per Basel III improved from 10.5% as at end-December 2017 to 11.4% as at end-September 2018 while total capital adequacy ratio also reinforced from 16.9% to 18.2% over the same period, both levels comfortably above the minimum regulatory ratios of 10% and 15% respectively. Liquidity remained also solid, representing 76.4% of customer deposits, a high level when compared to regional and global benchmarks.

20% year-on-year growth in net profits driven by revenues and cost efficiencies

Bank Audi reported in the first nine months of 2018 a 20% growth in consolidated net profits after provisions and taxes as compared to the net profits before discontinued operations in the corresponding period of 2017. Subsequently, consolidated net profits reached US$ 410 million, despite Odea Bank allocating its operating profits in the third quarter of 2018 to loan loss provision. The contribution of entities abroad reached US$ 132 million representing 32% of the total, of which US$ 51 million from Bank Audi in Egypt, US$ 42 million from Odea Bank in Turkey, US$ 21 million from entities in Europe and US$ 17 million from other MENA entities.

This performance results mostly from a 16.4% increase in net interest income and a 13.8% contraction in consolidated general operating expenses. The increase in net interest income included new taxes on financial investments in Lebanon for US$ 68 million over the same period. Consolidated spread expanded from 2.39% as at end-December 2017 to 2.74% as at end-September 2018 with the increase stemming in particular from Lebanese entities.

Consolidated general operating expenses decreased year-on-year by US$ 81 million, of which US$ 12 million in Lebanon and US$ 69 million in entities abroad. US$ 44 million of the latter represent the real decrease in expenses within a currency translation effect estimated at US$ 25 million. Subsequently, the cost to income ratio continues to improve gradually quarter on quarter reaching 43.8% in the first nine months of 2018 compared to 51.4% over the same period in 2017.

1.24% ROAA & 15.4% ROACE

Subsequently, the Group’s profitability metrics strengthened. The return on average assets improved to 1.24% as at end-September 2018 as compared to 1.06% as at end-December 2017; the return on average common equity increased from 13.4% as at end-December 2017 to 15.4% as at end-September 2018; and, the earnings per common share rose from US$ 1.03 in 2017 to US$ 1.25 on an annualised basis in the first nine months of 2018.

Bank Audi’s results underline the strong fundamentals of the Group and the diversified nature of its operations. 20% net income growth year on year reaching US$ 410 million and core tier 1 reaching 11.4% despite headwinds in certain geographies are the key achievements of the period. Bank Audi and its dedicated personnel remain committed to sustained shareholder value creation through premium facilitation of the banking needs of its customer base in its selected geographies, balanced growth and efficient deployment of resources.

Among Top Regional Banking Groups

LEBANON│SWITZERLAND│FRANCE│JORDAN│EGYPT│KSA│QATAR│MONACO│TURKEY│IRAQ│REP.OFF.IN ABU DHABI

https://www.zawya.com/images/features/181031-BAE.jpg

For more information:

Tamer Ghazaleh

Tel: +961 1 964 064

Group Chief Financial Officer

Email: Tamer.ghazaleh@bankaudi.com.lb

Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.

{kind=link}