PHOTO

The Islamic finance industry’s assets grew to $2.5 trillion in 2018 from $2.4 trillion in 2017, a rise of 3 percent, according to the Islamic Finance Development Report 2019.

This growth was slower than in previous years and was noticeable in some of the industry’s main markets where the wider economy is sluggish. Iran, Saudi Arabia and Malaysia were the largest markets of the 61 countries that reported Islamic financial assets, with all three recording more than $500 billion in assets, the report said.

While the top-ranked developed countries in Islamic Finance industry are Malaysia, Bahrain, the UAE and Indonesia, the countries which saw the fastest growth in assets were Morocco, Cyprus and Ethiopia.

Indonesia was one of the fastest-growing of the top 10 countries as a 37 percent increase in its IFDI score saw it jump from 10th position in the 2018 report to fourth in 2019, according to the study developed by ICD, the private sector development arm of Islamic Development Bank and global data provider Refinitiv.

Indonesia Islamic Finance Development Indicator (IFDI) score was boosted by a stronger performance in the Islamic finance Knowledge indicator, which takes into account education and research, and improvements in governance and awareness. Indonesian Islamic finance assets amounted to $86 billion in 2018, a rise of 5 percent from $82 billion in 2017, the report said.

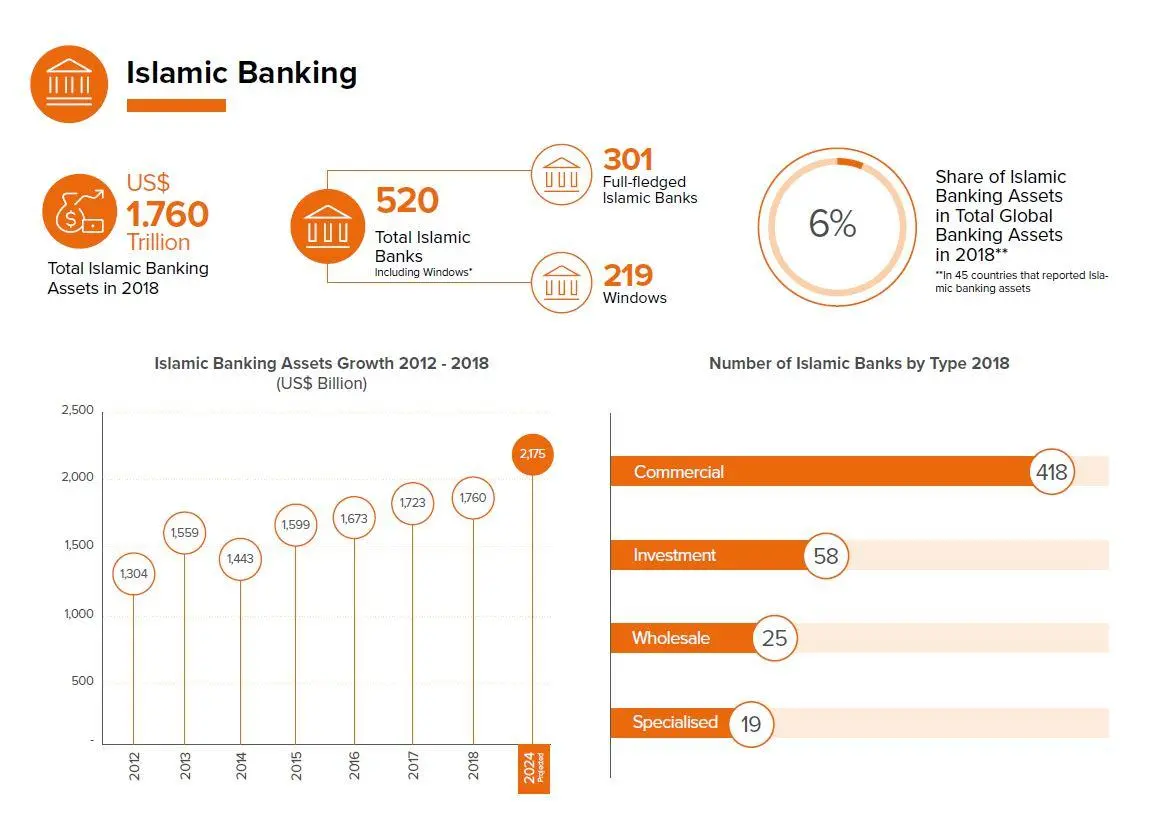

Islamic Banking

Growth in the industry’s leading sector, Islamic banking, slowed to 2 percent, largely in line with slowing growth for the global economy. Islamic banking assets totaled $1.76 trillion. Many Islamic banks or windows are also undergoing continuing transformation through either reorganization or consolidation.

Despite the slow growth, new banks and markets continue to enter the market, as seen in Ethiopia, Algeria and Afghanistan. Also, new liquidity tools are being developed to help grow existing Islamic banking markets, as seen in the UK and Pakistan, the report noted.

The Islamic banking sector in the GCC continues to be shaped by a wave of consolidation either between conventional banks with Islamic windows or between full-fledged Islamic banks.

Image courtesy Islamic Finance Development Report 2019

Meanwhile, new liquidity tools are expected to boost Islamic banking in UK and Pakistan.

The Bank of England in September 2018 announced the creation of a Shariah-compliant liquidity facility that for the first time will allow Islamic banks to hold sterling deposits at the central bank. This will

provide Islamic banks in the UK with greater flexibility in meeting Basel III liquidity requirements and put them on a level playing field with conventional banks.

The State Bank of Pakistan has launched three new Shariah-compliant refinance schemes to support banks in lending to small business, renewable energy, and agricultural projects. The facilities will be based on the risk-sharing mudaraba contract.

Takaful

Takaful and other Islamic financial institutions (OIFIs) account for the remaining share of Islamic financial institution assets with a respective $46 billion and $140 billion reported for 2018. Although, takaful grew a mere 1 percent and OIFIs even declined from 2017, both sectors are seeing transformational activities in their main markets that should lead to improved growth in coming years, particularly in Saudi Arabia and the UAE.

Moreover, both sectors are taking in new entrants in new markets. Developments in InsurTech and FinTech are also set to transform these sectors, the report said.

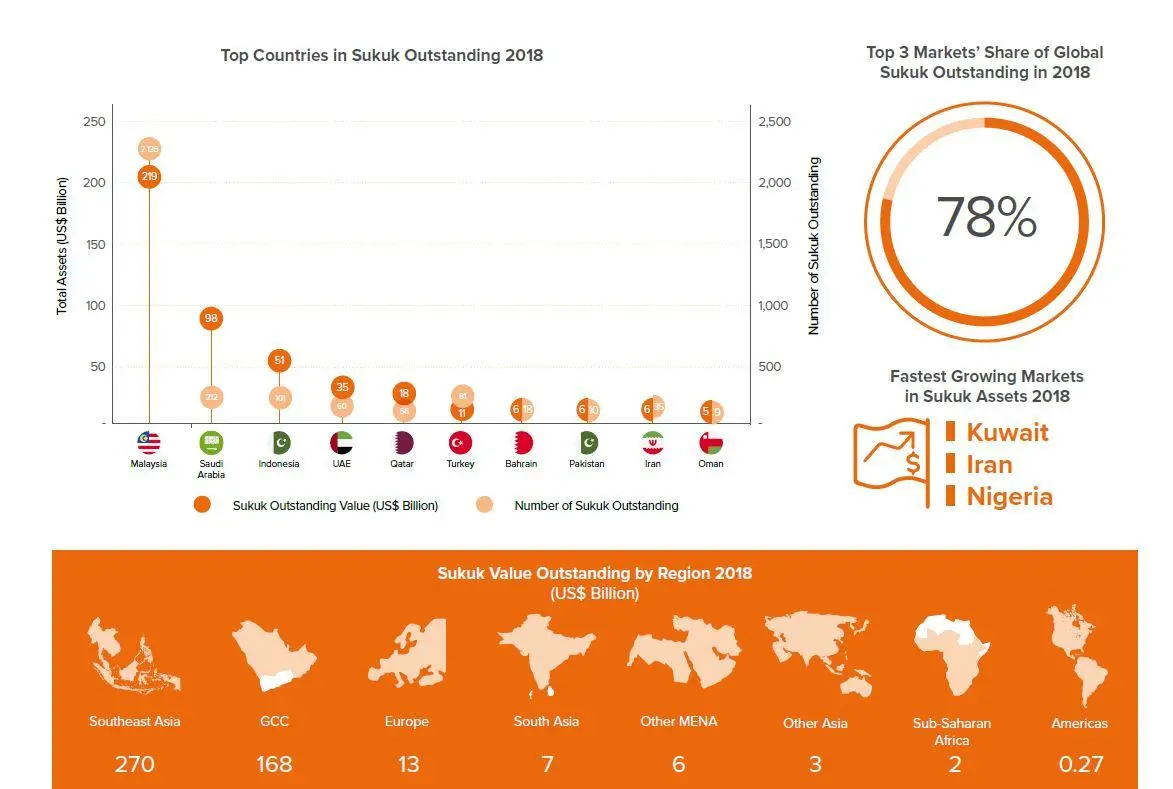

Sukuk market

In contrast with other sectors, the global slowdown did not impede the sukuk asset class from continuing its strong growth, rising 10 percent in 2018 to $470 billion.

Sukuk issuances during the year reached $125 billion, a similar figure to the previous year.

Sukuk market is developing the fastest in Saudi Arabia driven by a government sukuk program that also spurred greater corporate issuance.

Image courtesy Islamic Finance Development Report 2019

The government launched its sukuk program in 2017 to diversify funding in the state budget. It plans to raise $31.5 billion in 2019. The program has so far focused on developing the domestic sukuk market and as such the government has reduced issuing conventional sovereign bonds, the report noted.

Green sukuk issuance began in Malaysia in 2017 with the debut issuance by renewable energy company Tadau Energy. The first such issuance outside Malaysia came in 2018 when an Indonesian sovereign green sukuk raised $1.25 billion. A subsequent $750 million issue in 2019 made the Indonesian government the largest issuer of green sukuk to date. The trend continues to grow in 2019 with the first green sukuk issued in the GCC region by UAE-based Majid Al Futtaim Group.

New innovative sukuk forms and structures emerged in 2018 and 2019 such as waqf, blockchain-based and gold-based sukuk.

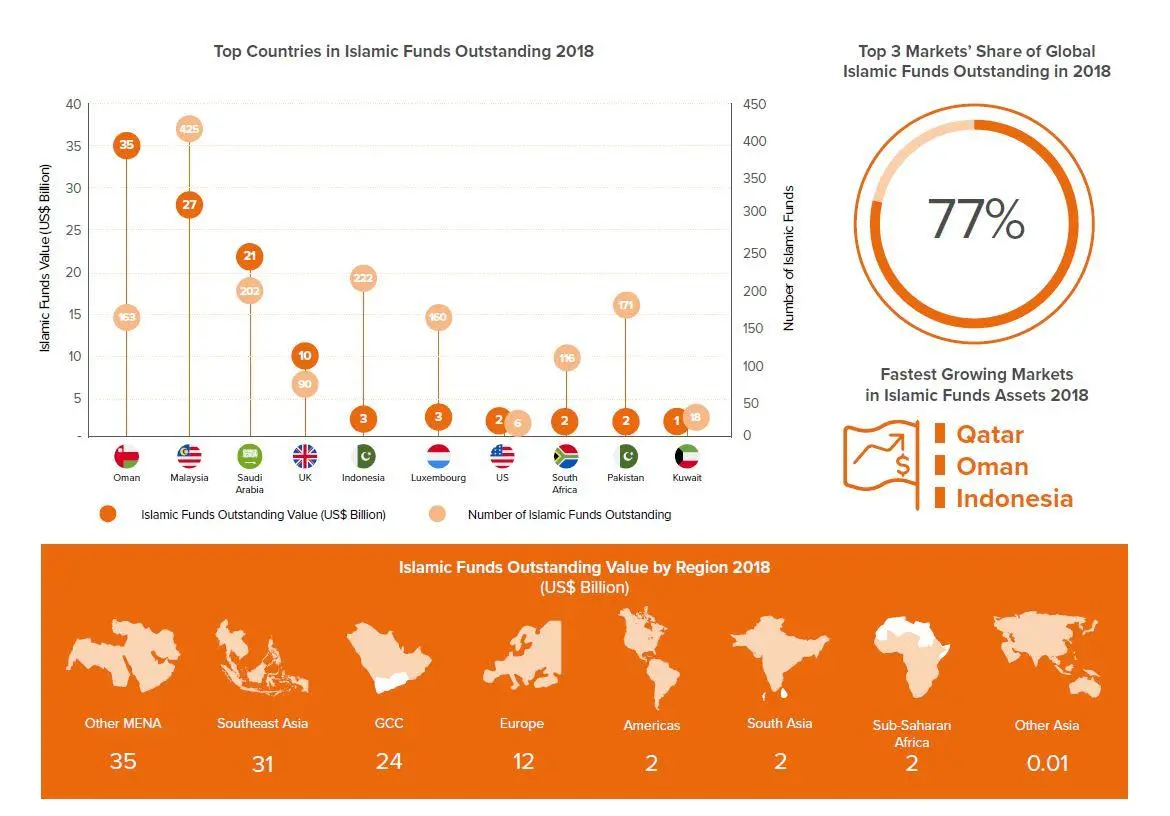

Islamic funds

Islamic funds, which had a strong performance in 2017, declined to $108 billion in 2018 as result of negative performances for most of the funds managed, in line with the global economic slowdown.

In fact, 2018 saw the weakest performance in Islamic funds in a decade.

Overall Islamic AuMs fell 10 percent during 2018, compared to 23 percent growth in 2017. This is mainly the result of subdued global economic conditions in addition to the poor performance of Asian equities during 2018.

Image courtesy Islamic Finance Development Report 2019

Malaysia and Indonesia are the two largest Islamic funds markets, and both their stock markets suffered losses in 2018. Iran, Malaysia and Saudi Arabia remained the largest Islamic funds markets, collectively accounting for 77 percent of global AuM.

Each saw a reduction in value of AuM during 2018. The UK and Indonesia have crept into the top five markets, replacing the US and Luxembourg.

(Writing by Seban Scaria seban.scaria@refinitiv.com, editing by Daniel Luiz)

Our Standards: The Thomson Reuters Trust Principles

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2019