The sudden and sharp trade recession lies at the root of the current global slowdown. In today’s integrated world with broadly diversified trade partners, open current and capital accounts, as well as tight international financial linkages, a trade shock directly impacts overall economic activity.

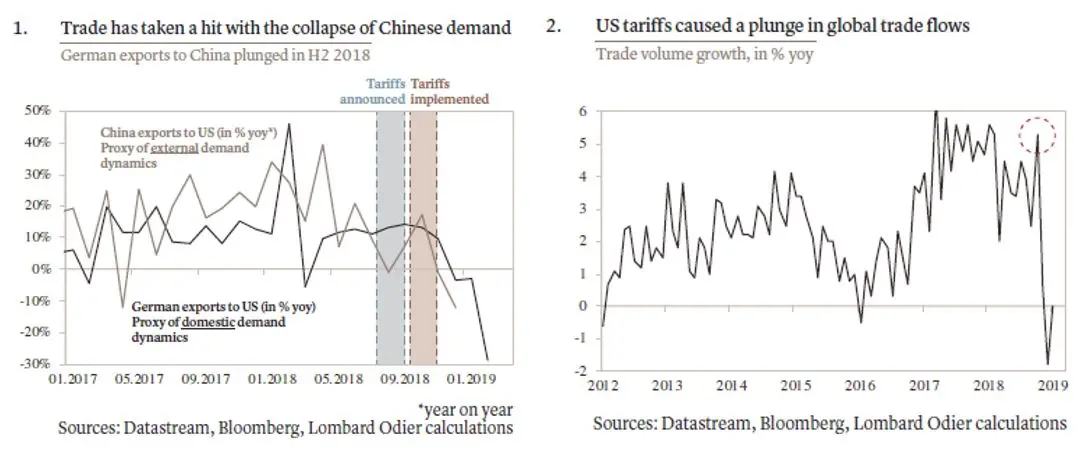

The good news is that the transmission channel should also work in the reverse direction. So, if the dispute between the United States and China gets settled and a solution to Brexit is found, a rebound in activity can be expected. Which is why our base case scenario for the coming quarters is one of global growth stabilisation, indeed even somewhat of a recovery. An improvement in the global trade outlook would be particularly favourable to Asia and Europe, where pressure from the external sector has weighed the most on economic trends (see charts 1 and 2).

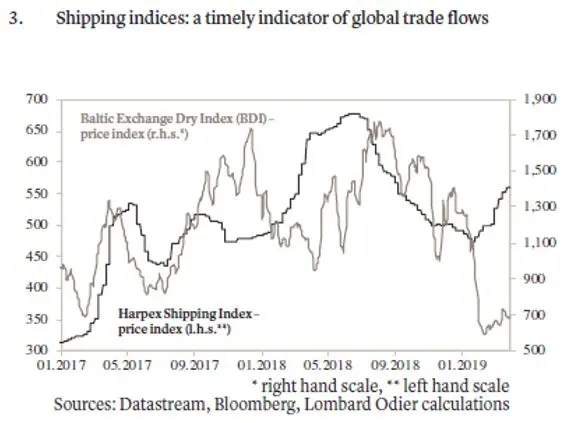

Although signs of improvement are slow to materialise, a number of activity indicators do offer some cause for optimism. The global manufacturing PMI stopped declining in March (unchanged at 50.6) and 75 percent of countries are above the 50 threshold (i.e. in expansion territory), the best ratio since November. The services component of the global PMI has progressed to 53.7, with 77 percent of countries in expansionary territory. The Harpex and Baltic Dry indices, which provide a timely measure of global container shipping activity, appear to be bottoming (see chart 3 – page 04). Finally, and more specifically, the Chinese pulse is starting to beat a little faster, with stronger credit growth and an encouraging rebound in the manufacturing PMI to an 8-month high of 50.8 (consistent with annual GDP growth around 6 percent). This improvement was then confirmed by a better-than-expected Caixin services PMI: at 54.4, it reached its highest level since January 2018.

We acknowledge that these green shoots are still fairly tentative and, to develop further, will require a trade deal between the U.S. and China. Only such a development would remove the uncertainty and allow confidence and activity to pick up more decisively. In the event that Chinese and U.S. negotiators do not come to terms, domestic demand dynamics in Europe and Asia, but also in the US, would be unable to defy external softness.

For now, discussions are moving in the right direction, with the damage already incurred from the trade war having incentivized both sides to find common ground. From a Chinese point of view, notwithstanding the ongoing transition towards domestic drivers, the economy remains very sensitive to trade flows. As for the U.S., even though exports have a lesser GDP weight, the global slowdown caused by the trade war has proved a major headwind for companies. This leaves us hopeful – albeit still vigilant, as the margin for policy missteps remains non-negligible – that a U.S./China deal will eventually be struck, involving no further increase in tariff rates and possibly also the removal of some of the existing ones.

With the Federal Reserve (Fed) taking a more dovish stance just a couple of weeks after the European Central Bank (ECB) decided to defer any potential interest rate hike to 2020 and announced the launch of a new series of targeted longer-term refinancing operations (TLTROs), the change in monetary policy trend is notable. Near-term risks of tighter financial conditions, that would have put the expansion at risk, have receded. Even though the aforementioned trade and Brexit issues still need monitoring, this more accommodative monetary stance represents a material change in the outlook. Not only should it help make the environment more predictable for a while, it could also serve to prolong the cycle.

To conclude, we would continue to point out that the current investment environment is unprecedented in many ways. The long-term theme of low Western world growth, combined with more immediate trade-related dangers, has led central banks to keep monetary conditions supportive for longer. The Fed has taken a pause in its tightening cycle even before reaching the neutral rate, and despite a full employment situation, while the ECB may struggle to ever normalise its rate policy. Our investment strategy continues to focus on making the most of this “low growth but easy money” context.

Any opinions expressed here are the author’s own.

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.